Sentiment analysis shows positive outlook in retail more opinion than fact

By Ross Guest and Ben Hachey

Heads of Australian companies are reasonably positive in their outlook for the rest of the year, according to our analysis of outlook statements of ASX top 100 companies, reporting results in the past month.

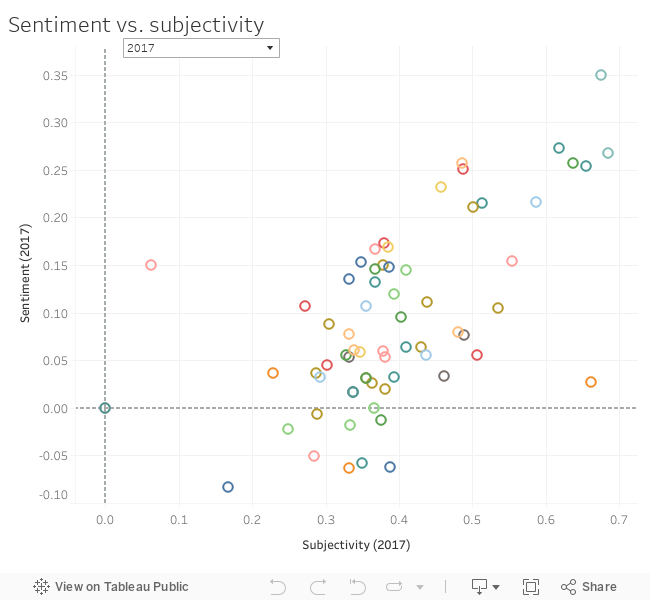

We used sentiment analysis to identify whether these statements were subjective and, if so, whether the opinions expressed are positive or negative. For the analysis here, we used a manually-crafted dictionary of sentiment keywords. Each keyword had a score for subjectivity and positive or negative sentiment.

So in terms of subjectivity score, numbers near zero indicate factual text and larger numbers indicate opinionated text. Sentiment ranges from -1 to 1 with smaller numbers indicating negative sentiment and larger numbers indicating positive.

We compared the outlook statements from February 2017 to those of the same month in 2016 and the sentiment was stronger in retailing than any other sector (chart below) and had doubled in strength since 2016 when it was not the strongest sector.

Strong retailing sentiment reflects households spending more due to low interest rates and some additional wealth generated from rising house prices. The job market has been steady, with unemployment falling slightly in January to 5.7%, although this was due to a rise in part-time rather than full-time jobs.

It seems that sluggish wage growth has apparently not hurt retailing sentiment – the wage price index, a measurement of wages, has struggled to keep pace with inflation, growing at 1.9% during calendar 2016 and likely to remain soft in 2017. Yet consumers have maintained their retail spending by cutting back their saving.

Leaders of companies in the pharmaceuticals, biotech, telecommunication and software sectors were positive again in 2017 with their outlook statements. This could be driven by long-term factors such as Australia’s ageing population and associated demand for medicines.

Those in the real estate sector were also positive this year and sentiment improved from 2016, this is likely to be driven partly by buoyant residential and commercial property markets. This is characterised by declining vacancy rates, rising demand for properties and supply constraints.

Sentiment was weakest in the utilities and energy sectors in 2017, this could be because of the market prospects for electricity, gas and oil. Difficulties in the electricity sector in terms of price and reliability of supply have become almost daily news, and policy uncertainty would contribute to the negative sentiment on what the year might bring.

Sentiment in the energy sector deteriorated from 2016 to 2017 reflecting the ongoing downturn in the oil and gas sector. Weak oil and gas prices are driven by long-term factors such as the boost in supply from the shale oil production and the growth in renewable energy supported by governments around the world. These factors are not going away any time soon.

In the outlook of banking and financial companies the sentiment has declined in 2017 relative to 2016, as the industry continues to be pressured by slowing credit growth, falling net interest margins and rising bad debts, as well as regulatory uncertainty.

It’s important to note the subjectivity of these outlook statements, whether they might represent opinions rather than objectively verifiable evidence. This could be an issue, for example, in the retail sector.

Some retail companies such as Harvey Norman and JB Hi-Fi scored the highest for subjectivity, indicating a lot of opinion in the outlook statements, despite the positive sentiment. Also a few oil and gas companies, with quite negative sentiment, also scored highly for subjectivity. One of the highest subjectivity scores was for Caltex.

Overall however, the positive sentiment in the recent company reporting season is consistent with a range of favourable macroeconomic drivers. The Australian economy is expected to grow by around 3% over the next two years.

Mining investment is expected to stop declining, at least if not rise, in the near future. The rise in commodity prices over the past six to 12 months is expected to hold up.

The election of US President Donald Trump and the British exit from the European Union (Brexit) inspired a bounce in stock markets, this reflects an optimism about the forecast economic impact of these events. In the case of Trump, an infrastructure and tax cut inspired boost to investment spending; and in the case of Brexit, more due to popular optimism about reclaimed sovereignty than rational evidence about real economic effects.

Other drivers include the low Australian dollar, at least lower by 28 per cent from the highest level in 2013. This helps make export and import competing sectors more competitive, which is reflected in a boost in exports and a rise in building and renovation activity. This is also driven by the prospect of ever-increasing real estate prices in our two largest capital cities.

The positive sentiment outlook here also resonates with a range of other positive business confidence analyses over recent months. The NAB business confidence survey in February reports positive and strongly improving business conditions. The Roy Morgan monthly business confidence index rose 2.4% in January.

The most recent Ai Group Indices for Services and Construction were both strong and indicate expansion of these sectors. And the Australian Chamber-Westpac survey of industrial trends strengthened at end 2016 by almost 5% from the previous quarter.

The above analysis is perhaps a glass half-full viewpoint. Yet we can also point to the ultimate forward looking indicator of the Australian economy – the Australian stock market – as further evidence of good times ahead. The All Ordinaries index of Australian shares was 5811 points on 8 March, an increase of 12% at the same date in 2016. That points to a positive outlook for Australian companies and therefore ultimately for all Australians through their wages, dividends earned by their superannuation funds, and taxes collected by the Australian government on behalf of all households.

rofessor of economics and national senior teaching fellow at Griffith University.

onorary associate in the School of Information Technologies at the University of Sydney.

This story first appeared on The Conversation.

Comment Manually

You must be logged in to post a comment.

No comments